- (937) 404-1040

- Mon - Fri: 8:30am - 5:00pm EST

Commercial Auto Insurance protects businesses that own, lease, or use vehicles for work. It is primarily liability insurance, but it can also include physical damage, medical payments, uninsured motorist coverage, hired and non-owned auto, and other endorsements.

This page focuses on small and mid-size business vehicles such as:

While trucking insurance is a specialized subset of commercial auto, most local contractors and service businesses fall under standard Commercial Auto policies. Cogo Insurance structures programs for contractors, HVAC companies, electricians, plumbers, landscapers, property managers, delivery services, manufacturers, and small fleets.

Commercial Auto Insurance is primarily liability insurance.

It pays for:

If your employee causes an accident while driving a company vehicle, the policy protects the business.

Liability applies whether the vehicle is:

FMCSA federal filings apply only to certain for-hire interstate motor carriers and specific hazmat or passenger operations.

The minimum federal public liability requirements are:

Entity Type | Vehicle Type | BIPD Insurance Requirement | Cargo Insurance Requirement | Surety Bond/Trust Fund Agreement | Applicable Form(s) |

For-Hire Property Carriers (Non-Hazardous) | GVWR < 10,001 pounds | $300,000 | $0 | $0 | BMC-91, BMC-91X, or BMC-82 |

For-Hire Property Carriers (Non-Hazardous) | GVWR ≥ 10,001 pounds | $750,000 | $0 | $0 | BMC-91, BMC-91X, or BMC-82 |

For-Hire Carriers of Certain Hazardous Materials | N/A | $1,000,000 | $0 | $0 | BMC-91, BMC-91X, or BMC-82 |

For-Hire and Private Carriers of Explosives, Poison Gas, or Radioactive Materials | N/A | $5,000,000 | $0 | $0 | BMC-91, BMC-91X, or BMC-82 |

For-Hire Carriers of Household Goods | GVWR ≥ 10,001 pounds | $750,000 | $5,000 | $0 | BMC-91, BMC-91X, BMC-82 and BMC-34 or BMC-83 |

Entity Type | Vehicle Type | BIPD Insurance Requirement | Cargo Insurance Requirement | Surety Bond/Trust Fund Agreement | Applicable Form(s) |

For-Hire Carriers of Passengers | 15 or Fewer Passengers | $1,500,000 | $0 | $0 | BMC-91, BMC-91X, or BMC-82 |

For-Hire Carriers of Passengers | 16+ Passengers | $5,000,000 | $0 | $0 | BMC-91, BMC-91X, or BMC-82 |

Important:

Even though FMCSA minimums can start at $300,000, most businesses carry:

Why?

Because landlords, municipalities, GCs, and commercial clients usually require $1,000,000. Minimum legal compliance and adequate risk protection are not the same thing.

Commercial Auto Insurance can also protect your own vehicles.

Pays for damage to your vehicle from an accident.

Pays for theft, fire, vandalism, hail, falling objects, and similar losses.

If your vehicles are financed, lenders require this coverage.

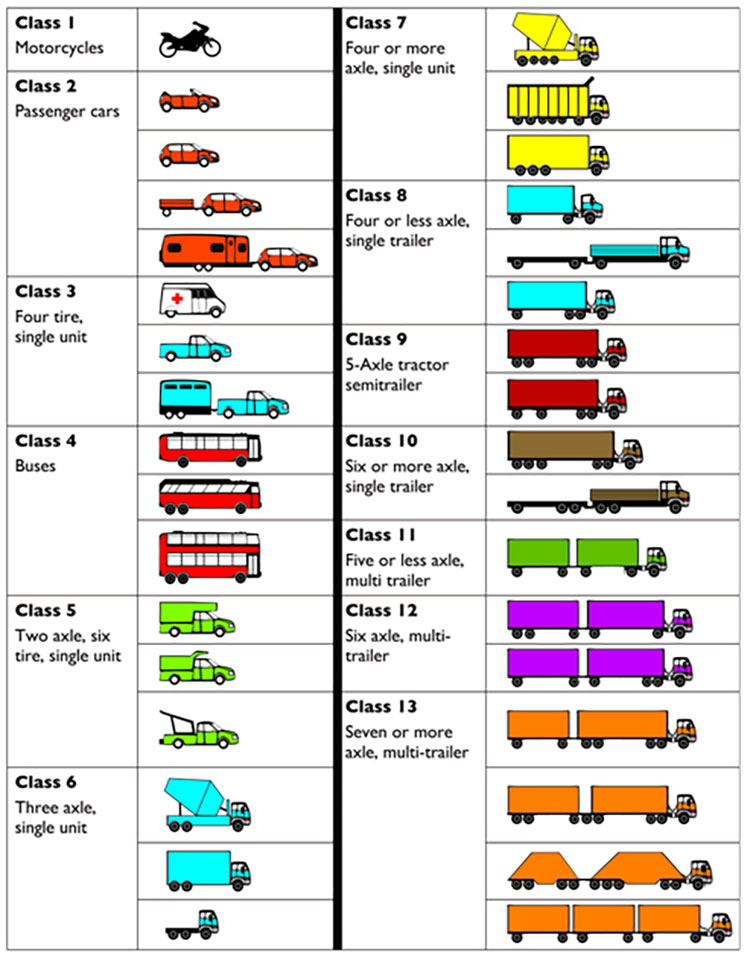

Many small and mid-size businesses operate medium-duty vehicles.

These include:

These vehicles create greater injury potential than passenger cars. Proper rating and classification are critical. Incorrect vehicle class or usage description can create underwriting problems or claim disputes.

Contractors frequently:

Commercial Auto Insurance protects the vehicle and liability exposure. Tools and equipment are typically insured under Inland Marine.

We structure coordinated coverage between:

Even if your business does not own vehicles, you may still have exposure.

HNOA covers:

HNOA can be added to:

Businesses without owned autos still need to evaluate this risk.

Serious accidents routinely exceed $1,000,000.

Commercial Umbrella provides additional limits above:

Common umbrella limits:

Auto liability is often the largest exposure in a business insurance program.

Commercial Auto Insurance for local businesses generally involves:

Trucking Insurance typically involves:

We evaluate operations carefully to determine the correct structure.

Premium depends on:

Medium-duty vehicles and longer radius operations carry higher rates.

Commercial Auto is often the largest liability exposure in a business program. Incorrect limits, misclassification, or failure to understand FMCSA vs local requirements can create serious problems.

We structure:

It may meet certain FMCSA minimums, but most contracts require $1,000,000. Risk exposure often justifies higher limits.

Yes, if vehicles are titled to the business or used primarily for work.

You need Hired and Non-Owned Auto coverage.

Yes, when used in business operations.

If vehicles are financed or valuable, yes.

If you operate as a for-hire interstate motor carrier, filings may be required. We evaluate this during underwriting.